As investors continue to pull money out of active funds and into passive funds, it is worthwhile to think about what the effect is on the markets. Without active investing, the market would not exist, as there would be nothing for indexed funds to follow. So, active investing will be around to some degree forever - but where is the breaking point?

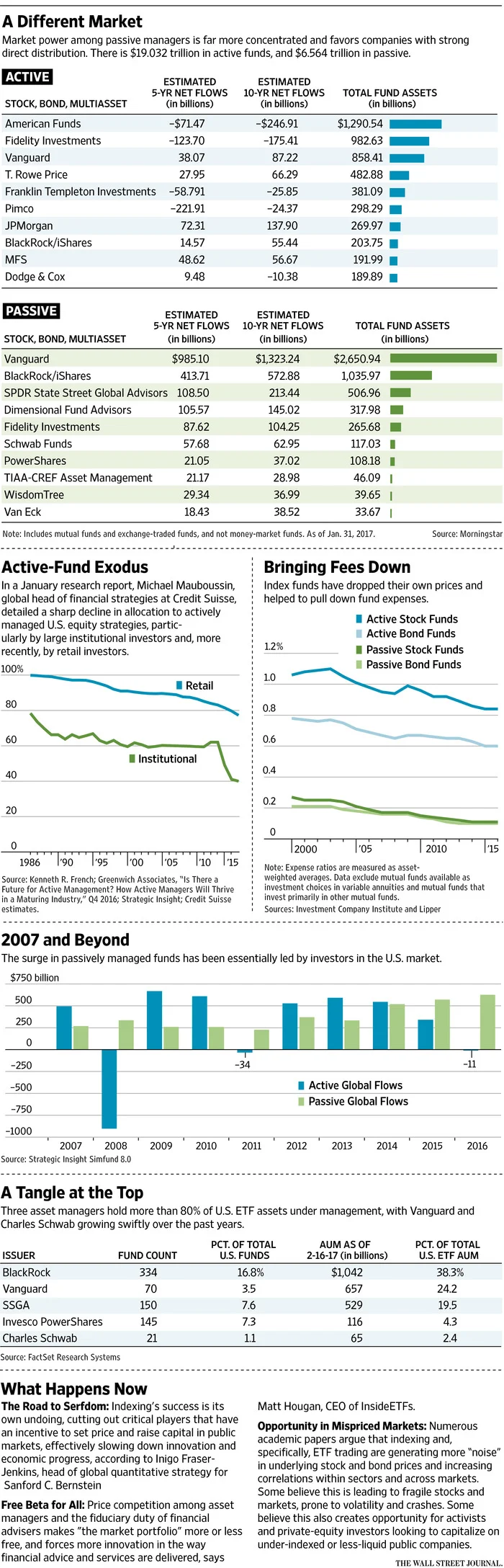

As larger companies grow larger and buy smaller companies, the number of publicly traded companies shrinks, as companies are going public more slowly than public companies are being bought. This will make active investing more difficult, as there are fewer choices to invest in. This Barron's article discusses the impact that passive investing has had on the market so far, and the expected continuing effects.

Firm governance has changed significantly as passive investing has become more popular. Firms such as Vanguard and State Street own a significant percentage of companies through their passively-managed funds, and generally tend to vote with management. Although this is not always the case, it makes it more difficult for shareholders to have their voices heard on important issues. Vanguard owns over 6% of the S&P market cap.

I believe in both passive and active management. I believe in passive indexing for efficient markets, such as US and developed large-cap markets. I believe in an active approach for those markets that are less efficient, such as fixed income and alternatives. I tend to invest in the companies that I know - which is definitely a biased approach - but it has worked so far. An avid TJ-Maxx shopper, I understand how their business model is so successful, because I want those deals. As a bi-monthly Costco shopper, I understand why the parking lot is packed before the doors have even opened on Sunday morning. So, I enjoy investing in those companies that I understand, too.

Overall, the most important thing is to have a diversified portfolio, and to at least put cash to work in this market that never seems to go down.